Chapter 1 – Exploring the Realm of Derivatives: Futures, Options, and Their Evolution

by Admin /

August 13, 2024 /

Beginner

Derivatives are financial contracts whose value is derived from an underlying asset. They enable investors to speculate on price movements, hedge risk, and manage exposure. Derivatives play a crucial role in financial markets, providing flexibility and liquidity for various investment strategies.

They serve as contracts between parties, traded on exchanges or over the counter. Prices are driven by fluctuations in underlying assets, such as stocks, bonds, currencies, and commodities. Derivatives enable risk mitigation through hedging or speculation on price movements.

Understanding derivatives is essential for investors, offering opportunities to manage risk and enhance portfolio returns. Futures and Options are Derivatives.

Let’s return to your school memories to revive and explain this in a real-world context. You must’ve come across the Density formula in physics.

Density = Mass / Volume

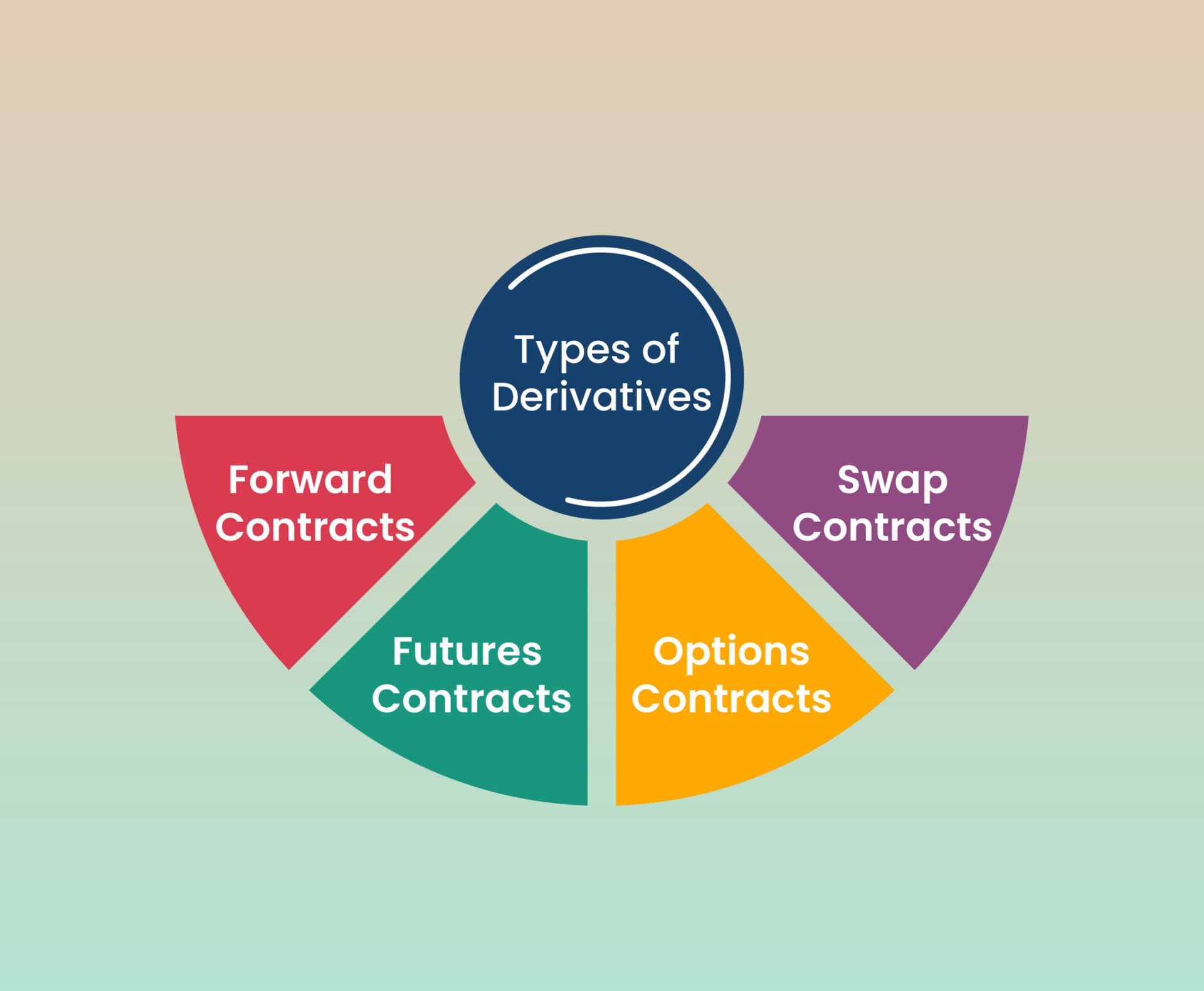

Types of Derivatives

In India, derivatives trading encompasses four main types, each with distinct characteristics:

Forward Contracts: These involve two parties agreeing to buy or sell an asset at a predetermined future date and price. Customized to each agreement, forward contracts carry high counterparty risk and settle upon maturity without collateral.

Futures Contracts: Similar to forward contracts, futures are standardized agreements traded on exchanges. Counterparty risk is lower as clearinghouses act as intermediaries. Fixed sizes and expiry periods make futures easily regulated.

Options Contracts: Different from futures, options provide the right but not obligation to buy (call) or sell (put) an asset at a set price. Call options grant buying rights, while put options grant selling rights. Traders can take long or short positions in either type, settling before expiry.

Swap Contracts: Swaps are intricate agreements privately arranged between parties. They involve exchanging future cash flows according to predetermined formulas. Typically involving interest rates or currencies, swaps protect parties from specific risks and aren’t traded on exchanges, often brokered by investment bankers.

Forward Contracts

The traces of the first Forward Contract dates back to the 18th century BC. King Hammurabi, who ruled the Babylon city, developed his influential code of law during his time. Forward contracts were mentioned among them for the first time in human history.

Futures are the modified forms of Forward Contracts. They are contracts to buy or sell an asset at an agreed price on a future date, used for speculation and hedging.

What is Futures?

Futures contracts are standardized agreements to buy or sell assets at predetermined prices and dates, traded on futures exchanges. Buyers commit to purchasing, while sellers commit to delivering the underlying asset. Used for speculation or hedging, futures allow investors to leverage positions on various assets like commodities or securities.

Regulated by the Securities and Exchange Board of India (SEBI) in India, they provide a way to manage price risks in markets. Unlike forward contracts, futures are exchange-traded, ensuring liquidity and standardization. These contracts play a crucial role for commodity producers, consumers, traders, and investors in managing and leveraging market positions.

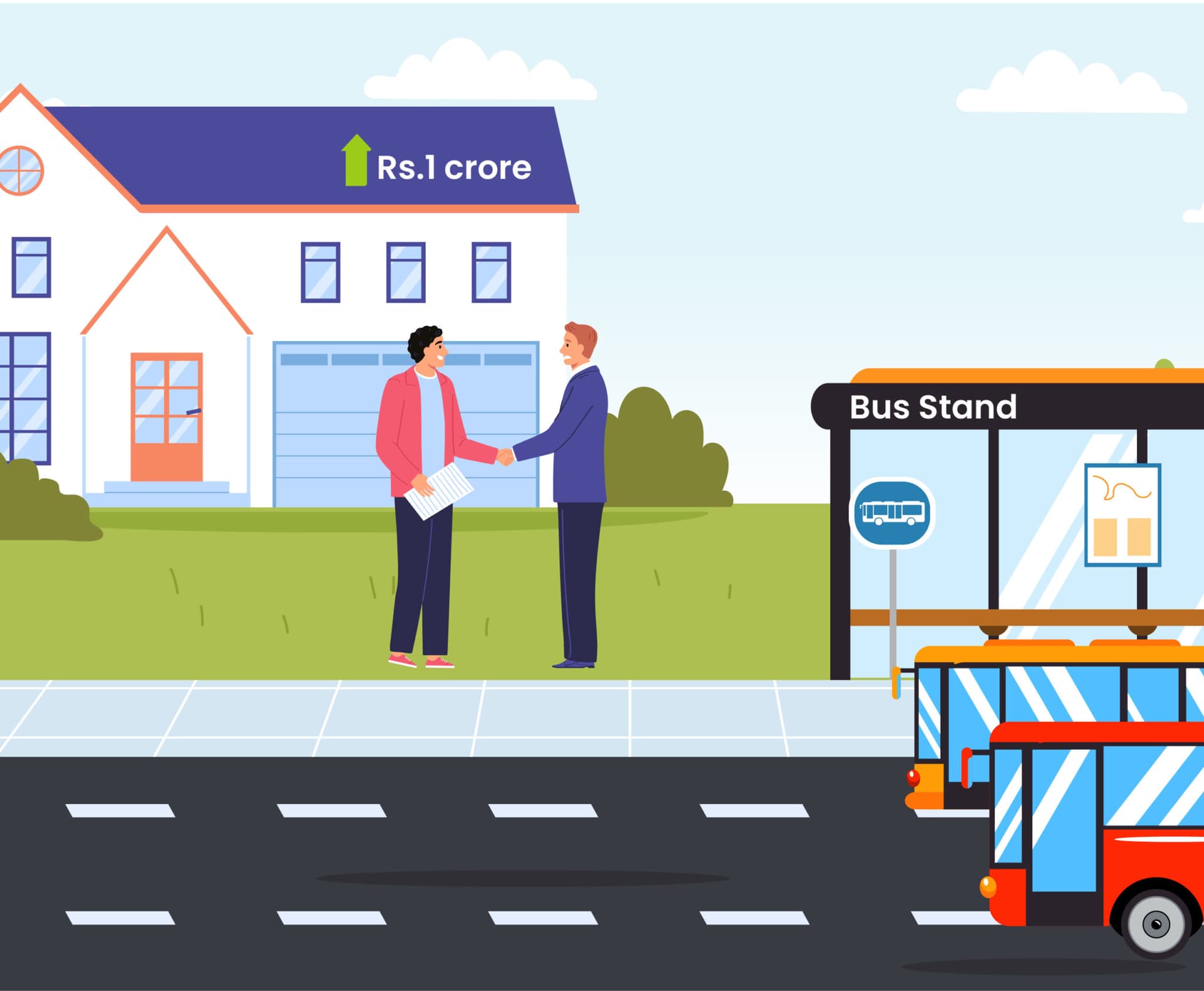

Let’s look at how this works with an example. You are a property investor who wants to buy a piece of land because you think in the next six months, the city bus stand is likely to get relocated to this area. If that happens, the property price will skyrocket drastically. On the 1st of January, you make a deal with a landowner to buy a property for Rs.75 lakh in the next six months, which is the 1st of July. This is called a Forward Contract. On the 1st of July, whatever the price of land will be and whether the bus stand gets relocated or not, you and the landowner are bound to honor the contract.

Let’s evaluate the perspectives of both parties. The landowner believes that the price of the land may go below Rs.75 lakh in the next six months, and that’s why he wants to seal the deal at today’s market price. On the other hand, you anticipate the price of the land to increase drastically in the coming months, and that’s why you’ve locked the price at Rs.75 lakh to profit from it.

Now that a contract is made, let’s look at three potential outcomes of it.

In Scenario 1, the price of the land goes up to Rs.1 crore. The investor, who has made a deal before 6 months, gets to buy the land for Rs.75 lakh, making a profit of Rs.25 lakh. On the other hand, the landowner loses the chance to sell the land at the current market price due to the contract.

Under scenario 2, the value of the land remains the same. Neither the property investor nor the landowner makes a profit from it.

But in scenario 3, the land price goes down to Rs.50 lakh. Because of the contract, the property owner is bound to buy the land at a higher price than the current market price. He loses Rs.25 lakh, while the landowner makes a profit from it.

So why do we need a ‘Futures’ contract in this scenario? Because every situation carries its own set of risks. In the above-mentioned scenario, there are a few things that could go wrong during the deal. For example, when the property investor wants to make a Forward deal, there could be no landowners willing to do so. Or the person who makes a loss in the deal might walk away, defaulting on the payment. There are chances that people could use it as a way to scam others if there is no regulatory body. The people involved might think of changing their stance in the third or fourth month.

Futures is introduced here to give a safety net to eliminate the risks associated with the contract. In summary, Futures are modern Forwards with a plethora of features like matching the buyer and seller and creating a standard contract. They are also regulated by the Securities and Exchange Board of India (SEBI). The contracts are time-bound, easily tradable, and cash-settled.

Elements of Futures Contracts

There are a few things that contain a Futures contract—Underlying, Margin, lot size, and expiry. Let’s consider the scenario in the Futures Contract chapter and define the values.

Underlying - Land

Lot size - 1 (sincehe no of land here is 1)

Expiry - 1st July 23

Margin - Rs.0

While the previous scenario doesn’t mention any exchange of money at the start of the deal, usually, people involved in the Futures are bound to pay a Margin (a percentage of the deal) to seal the contract. This is to cover the potential loss that could happen to any party.

What are Options Contracts?

Just like futures contracts, options contracts are deals between two parties to possibly buy or sell a security at a specific price, known as the strike price, by a certain date.

There are two types of options contracts: puts and calls. Calls are bought when you think a security will go up in value, while puts are bought when you think it will go down. Call buyers have the right to buy shares at the strike price, while put buyers can sell shares at the strike price.

Option sellers, or writers, have to follow through if buyers decide to use their options. With a call option, sellers get paid a premium to sell shares at the strike price, either right away (if they already have the shares) or later. Put buyers bet on the price dropping and have the right to sell shares at the strike price. If the price goes down, they can sell the shares at the strike price or sell the option itself.

Important Instances in the History of Options Trading

Here are some of the important instances in the history of Options trading.

The earliest record of Options can be found in a book written by Aristotle in the mid-fourth century BC. Due to insufficient funds to own all the olive presses, Aristotle paid some money to the owner and secured the rights to use them at harvest time.

Another relevant occurrence of Options happened during the Tulip Bulb Mania. While the price of tulip bulbs increased during the 1630s, the value of the Options contracts also went up. When the bubble burst, there was no way to force investors to fulfill their obligations due to lack of regulation.

A significant milestone in the history of options trading was marked by the actions of an American financier named Russell Sage. During the late 19th century, Sage initiated the creation of over-the-counter call and put options for trading in the United States.

Upon its initial trading commencement, the CBOE featured a limited number of listed contracts, exclusively comprising calls. Puts had not yet been standardized during this period.

There were still unsettling difficulties around calculating a fair price of an Option. Eventually, two professors named Fisher Black and Myron Scholes, devised a mathematical formula to calculate the price of Options using specified variables. The formula known as the Black-Scholes Pricing Model still has a major impact on the industry.

When online trading began to gain popularity towards the end of the 20th century, Options became easily available and accessible to the general public.

FAQ's

What are derivatives in the stock market?

Derivatives are financial contracts whose value is derived from an underlying asset, such as stocks, indices, commodities, or currencies. They are primarily used for hedging risk, speculation, and gaining leverage.

What are the main types of derivatives?

The most common types of derivatives are futures, options, forwards, and swaps. In the stock market, futures and options (F&O) are the most widely used.

Why do investors use derivatives?

Investors use derivatives to hedge against market risk, speculate on price movements, and enhance portfolio performance with lower capital outlay through leverage.

Are derivatives suitable for beginners?

Derivatives can be complex and carry higher risk due to leverage. However, with proper education (like NxtOption's Learn section), beginners can gradually understand and use them effectively.

How are derivatives traded in India?

In India, derivatives are traded on exchanges like NSE and BSE. The most popular instruments include index derivatives (like Nifty and Bank Nifty futures & options) and stock derivatives.